Digital advertising, which accounted for 51% of India’s ad market in 2024, surpassed traditional advertising last year. In 2025, digital ad spending is projected to grow by 12% to reach Rs 728 billion ($8.4 billion), while revenue from traditional media is expected to rise by 3.4% to Rs 643 billion ($7.5 billion), as per IPG Mediabrands’ latest MAGNA report.

The IMF has projected global growth at 2.8% in 2025, with India’s growth forecasted at 6.2%. In 2026, India is projected to grow by 6.3%.

As per the report, India has overtaken Japan to become the 4th largest economy in 2025 and will leave behind Germany to become the 3rd largest market in 2028. India is well placed to deal with global trade disruptions supported by robust internal growth drivers.

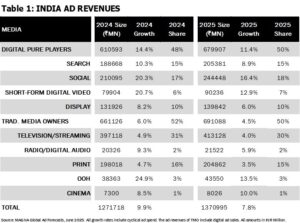

Total Adex is estimated to grow +7.8% in 2025 to reach Rs 1,371 billion ($15.9 billion). In 2026, by +7.7%. The report also highlighted that social advertising is advancing to be the largest format and is expected to overtake television in the next five years.

Overall, India’s economic outlook remains positive, with robust growth potential supported by a combination of domestic demand, government investment, and a thriving services sector. In a high-stake election year (2024), the market grew +6.5%. IMF in its April 2025 report, projects a slight contraction in activity with a growth forecast of +6.2% in 2025 and a marginal recovery with +6.3% expansion in 2026.

Monetary tightening of the past is now being rolled back by the central bank, paving way for recovery. With the inflation cooling from 4.7% in 2024 to estimated 4.2% in 2025 and 4.1% in 2026, the central bank is signalling staunch support for economic revival with front loading interest rate cuts and injecting liquidity into the market.

The evolving global trade landscape is expected to influence India’s growth trajectory and potential trade headwinds could have an impact on the economy. However, India is well placed to manage the effects of trade disruptions because of domestic growth drivers and low dependence on exports. Nonetheless, the key sectors that drive both trade and domestic adex such as CPG, Auto, Textiles, Electronics and Tech face challenges and India maintains an extremely cautious stance.

The Media Owners revenue outlook in 2025 is positive across both linear and digital formats. 2025H1 will see an increase of +6% and the latter half of the year will grow +9%. Any impact of trade is likely to be felt in the second half of the year and though our full-year forecast accounts for this challenging environment, the situation is still forming and there is uncertainty.

The YOY growth of +7.8% in 2025 with total revenue increasing by Rs 99 billion taking the total adex from Rs 1,272 billion ($14.7 billion) to Rs 1,371 billion ($15.9 billion). Digital Pure Player formats valued at Rs 680 billion ($7.9 billion) are driving the advertising economy, which is estimated to grow at +11.4%.

Video (Rs 413 billion, $4.8 billion) which is the second largest format is estimated to grow +4%. While Digital Video growth is +17%, overall video spends are weighed down by linear television which is forecast to grow +2.5%. Digital Pure Play and Video accounts for 80% of the total adex. Publishing (INR 205 billion, $2.4 billion) will grow +3.5% with the digital version of the format growing at twice the rate. Audio and Experiential, which is 5% of the adex, will be growing at +5.9% and +12.9% respectively. In 2026, the growth is expected to be +7.7%.

Hema Malik, Chief Investment Officer, IPG Mediabrands India, said, “MAGNA predicts above average ad spend resilience in 2025 neutralizing the impact of ad spend on cyclical events in 2024 led by National Elections & T20 World Cup. In 2025 MAGNA expects dynamic ad spend in Finance, Media, Pharma, Technology, Gaming and Retail, while Automotive and Electronics might lag. The trio of Video, Social and Retail will once again lead the Adex growth. Live sports, which were the only Linear TV mainstays, have been upended with more people streaming sports content. Ad-supported streaming experiences rapid growth in access, consumption, and advertising sales, as nearly all streaming TV platforms offer more affordable ad-supported plans. Long-form video is growing at a blistering pace of over +25% and is 6% of the total video forecast, estimated to gain double digit share in the next three years.”

{kind=link}