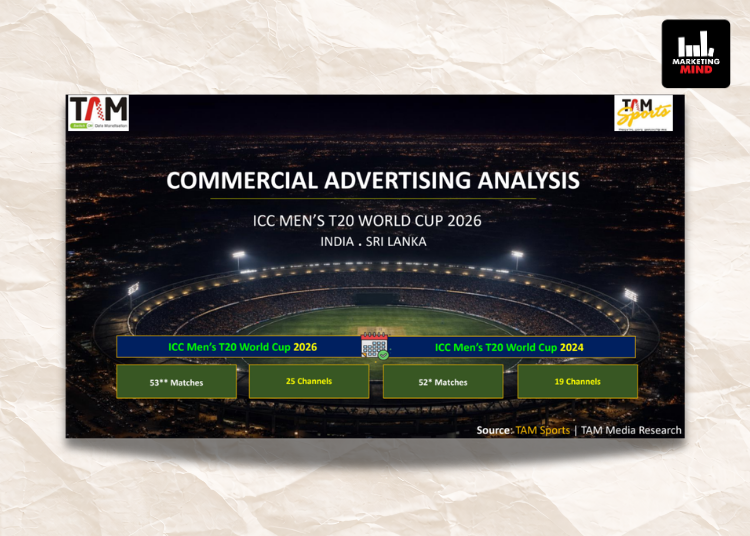

The report has shown that matches featuring India have delivered 66% higher ad volumes than non-India matches, underscoring the country’s influence on advertising demand during global cricket tournaments.

At the same time, advertiser participation has declined significantly. The number of categories, advertisers, and brands has dropped by 55%, 63%, and 66% respectively compared to 2024, indicating a more concentrated advertising landscape.

Ad volumes during the final have increased by 18% compared to the previous edition, reflecting stronger monetisation in high-impact matches. The Super 8 stage has also recorded a 48% rise in ad volumes per match, pointing to increased advertiser focus during advanced stages of the tournament.

Category-wise, Cars has emerged as the leading segment with a 15% share of ad volumes, followed by E-commerce services at 14%. The top five categories have contributed 53% of total ad volumes, indicating growing concentration among leading sectors.

Among advertisers, OpenAI has led with a 12% share of ad volumes, followed by Coca-Cola India at 9% and Mahindra & Mahindra at 8%. The top five advertisers have collectively contributed 39% of total ad volumes, consistent with the previous edition, though there has been no overlap in the top five advertisers between 2024 and 2026.

The top five brands have also shown a complete shift compared to the previous edition, contributing 30% of total ad volumes in 2026.

In terms of ad formats, 11–20 second ads have dominated commercial breaks, followed by ads under 10 seconds, indicating a preference for shorter-duration advertising.

{kind=link}