The Indian Media & Entertainment sector has grown by over 8% in 2023 to cross Rs 2.32 trillion, as per the latest edition of the annual FICCI-EY report. This year, the same is predicted to grow by 10.2% to cross Rs 2.55 trillion, with the two industry bodies predicting that digital medium would overtake television as the largest segment.

“We expect the M&E sector to grow 10.2% to reach INR2.55 trillion by 2024, then grow at a CAGR of 10% to reach INR3.08 trillion by 2026,” the report mentioned.

As per the report, while the sector was 21% above its pre-pandemic levels in 2023, television, print and radio still lagged their 2019 levels and that TV, which happens to be the largest segment, is likely to be overtaken by digital media in 2024.

When comparing the segment growth of 2023 with the previous year, i.e.- 2022, the report mentions that the growth of Rs 173 billion was driven by New Media and that TV was the only medium which saw a decline of 13%.

Remaining mediums such as Music (2%), Radio (2%), OOH Media (5%), Animation & VFX (7%), Print (10%), Live events (15%), Filmed entertainment (24%) and Online gaming (39%) all grew together.

According to EY estimates, the growth of Rs 173 billion was half of the INR 371 billion growth that took place in 2022, mainly due to headwinds in advertising during the first half of the year.

“New media (digital and online gaming) grew the most, providing INR 122 billion of the total growth, and consequently, increased its contribution to the M&E sector from 20% in 2019 to 38% in 2023. The share of traditional media (television, print, filmed entertainment, live events, OOH, music, radio) stood at 57% of M&E sector revenues in 2023, down from 76% in 2019,” the report mentioned.

Additionally, as per the report, advertising was impacted by a ban on certain large and high-yield categories like gaming and betting, and a slowdown in investments in D2C brands and therefore, advertising is now 0.33% of India’s GDP.

Experiential (outside the home and interactive) segments continued their strong growth in 2023, and consequently, online gaming, filmed entertainment, live events and OOH media segments grew at a combined 18%, contributing 48% of the total growth, the report mentioned.

As per EY estimates, Television advertising fell 6.5% due to a slowdown in spending by gaming and D2C brands, which impacted revenues for premium properties.

“The HSM market was also soft, resulting in a 3% overall ad volume de-growth. Subscription revenue grew after three years of fall on the back of price increases, though pay TV homes fell by two million. While linear viewership grew 2% over 2022, 19 to 20 million smart TVs connected to the internet each week, up from around 10 million in 2021,” the report mentioned.

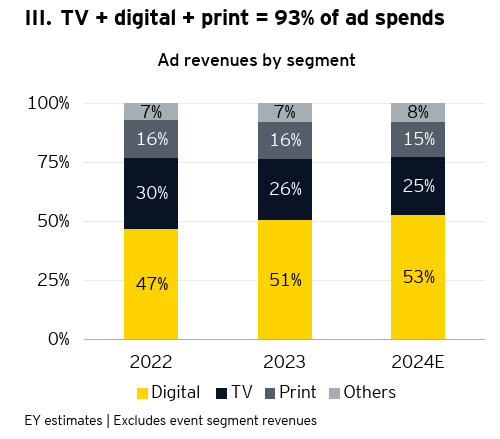

That being said, Digital advertising grew 15% to reach Rs 576 billion, or 51% of total advertising revenues (included in this is advertising by SME and long-tail advertisers of over Rs 200 billion and advertising earned by e-commerce platforms of Rs 86 billion).

Similarly, Digital subscription also grew 9% to reach Rs 78 billion, which is a third of 2022’s 27% growth, as premium cricket properties were moved in front of paywalls.

“Paid video subscriptions reduced by two million in 2023 to 97 million, across 43 million households in India. Paid music subscriptions grew from 5 million to 8 million, generating INR 3 billion while online news subscriptions generated INR 2 billion,” the report mentioned.

Furthermore, the FICCI-EY report also pointed out that bucking the global trend, print continued to thrive in India as advertising revenues grew 4% in 2023, with a notable growth in premium ad formats, as print remained a “go-to” medium for more affluent and non metro audiences. On the other hand, subscription revenues also grew 3% on the back of rising cover prices and digital revenues were insignificant for most print companies.

“Online gaming segment’s growth slowed to 22% in 2023 to reach INR 220 billion. It overtook filmed entertainment to become the fourth largest segment. There were over 450 million online gamers in India, of which around 100 million played daily. We estimate over 90 million gamers paid to play; real money gaming comprised 83% of segment revenues. Impact of a higher GST levy was largely absorbed by larger players, impacting margins, but protecting growth,” the report added.

As per EY estimates, the film segment also grew 14% to reach Rs 197 billion as over 1,796 films were released in 2023, and theatrical revenues reached an all-time high of Rs 120 billion and number of screens grew 4% and fewer films released directly on digital platforms.

“The Hollywood writers’ strike impacted global supply chains, and consequently, the Animation and VFX segment grew just 6% in 2023. Potential mergers and falling ad revenues also reduced the slate of animated content produced for broadcast in India. A revival in demand in the second half of the year led to growth, boosted by the trend of using more VFX in Indian content,” it mentioned.

The organized Live events segment, as per FICCI-EY report, grew 20% to finally exceed its pre-pandemic levels. Growth was driven by government events, personal events and weddings, and ticketed events, including several international formats.

Another media which grew in double digits- at 13% in 2023 and crossed its 2019 levels was OOH. As per the report, premium properties and locations led the growth and Active digital OOH screens crossed 100,000 and contributed 9% of total segment revenues.

“The Indian music segment grew by 10% to reach INR 24 billion in 2023, slower than previous years as certain music OTT platforms went pay and stopped or reduced their free services. 87% of revenues were earned through digital means, though most of it was advertising led on YouTube, there being around only 8 million paying subscribers despite music streaming’s reach of 185 million,” the report stated.

Similarly, Radio segment revenues also grew 10% in 2023 to Rs 23 billion on the back of more retail and local advertising, and alternate revenue streams, as per FICCI-EY report.

“Ad volumes increased by 19% in 2023 as compared to the previous year, though ad rates remained below their 2019 levels,” the report added.

Sharing the highlights of the report, Kevin Vaz, Chairman, FICCI Media and Entertainment Committee, said,

“The integration of digital technologies in the Indian M&E sector is at a scale without parallel amongst the comity of nations. The sector is witnessing a massive transformation, fuelled by the Government of India’s thrust on improving digital infrastructure in the country. In 2024, digital media is poised for explosive growth, potentially overtaking television to become the leading segment of the M&E sector. This surge in digital media is forecasted to propel the M&E sector’s growth to a 10% annual rate, crossing INR3 trillion ($37.1 billion) by 2026. This growth is buoyed by a robust digital infrastructure, widespread adoption of OTT platforms, significant growth in the gaming segment, and the availability of cost-effective options for consumers. Despite this digital boom, traditional media is also experiencing steady growth and thus India is a “Linear and Digital Market” rather than “Linear or Digital Market”. This resilience also serves as evidence of the enduring relevance of print, radio, out-of-home advertising, and regional television, illustrating India’s diverse media consumption habits.”

He also added, “The 2024 Report encapsulates the spirit of resilience, innovation, and collaboration that are the hallmarks of our M&E sector. As we navigate towards a bright and dynamic future, it is crucial to leverage the synergy of creativity and technology with forward-looking policy and regulatory regimes. This can position India as the content hub of the world – bringing its unique stories, rich culture, and diverse perspectives to the global stage.”

Click here to view the full report.

{kind=link}