What is a No Cost EMI?

You might have seen on various shopping websites like Flipkart, Amazon, etc. a No Cost EMI payment option. This is the mode of payment that enables you to pay for your article in installments without paying any extra charges in the form of interest.

No cost EMI basically means that the lender and the retailer are offering you the EMI facility at zero processing fees and zero interest. So you pay only the actual price of an item but instead of a lump sum payment, you pay in EMIs over 3–12 months.

But do note that the EMI payment option normally incurs a certain interest. It is only when NO Cost EMI is mentioned you will not be charged any interest by these online aggregators.

So Who Bears The Interest Charges?

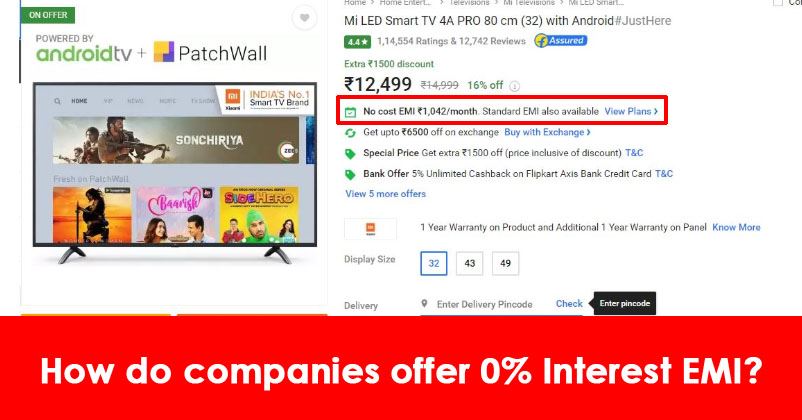

Recently, we tried buying an MI LED smart television online. The price of the product was mentioned as Rs. 12,499.

Then we proceeded to select the No EMI option & selected a 9 months payment option.

Just when you choose the plan and proceed to enter your card details, there is a terms & condition popup. When we selected that we read something people normally miss out.

It said, “If you pay using a credit card eligible for No Cost EMI, a discount equal to the interest payable to the bank is provided to you upfront at the time of payment. Please note however that this discount is offered by brands and you will be required to pay EMI & interest to bank on the total order value. Your bank might charge GST on the interest amount which might be visible on your statement. This GST amount, however, will not be included in the No Cost EMI discount.”

Also, when we tried buying another item through Flipkart we came across this disclaimer.

The interest amount was included in the product’s price already which was of INR 7999. And when we proceeded with making the payment it showed that the product amount is INR 7613 which will be blocked on our cards & INR 386 is levied as Interest on EMI given to the bank.

As per these online websites, the interest charges are actually borne by them. The charges are added in the products final price and we pay what we were promised at the beginning. And they are the ones who pay the bank the interest.

So you see, the bank will get their interest at the end. One way or another, the due interest amount is given to the bank once the payment is initiated.